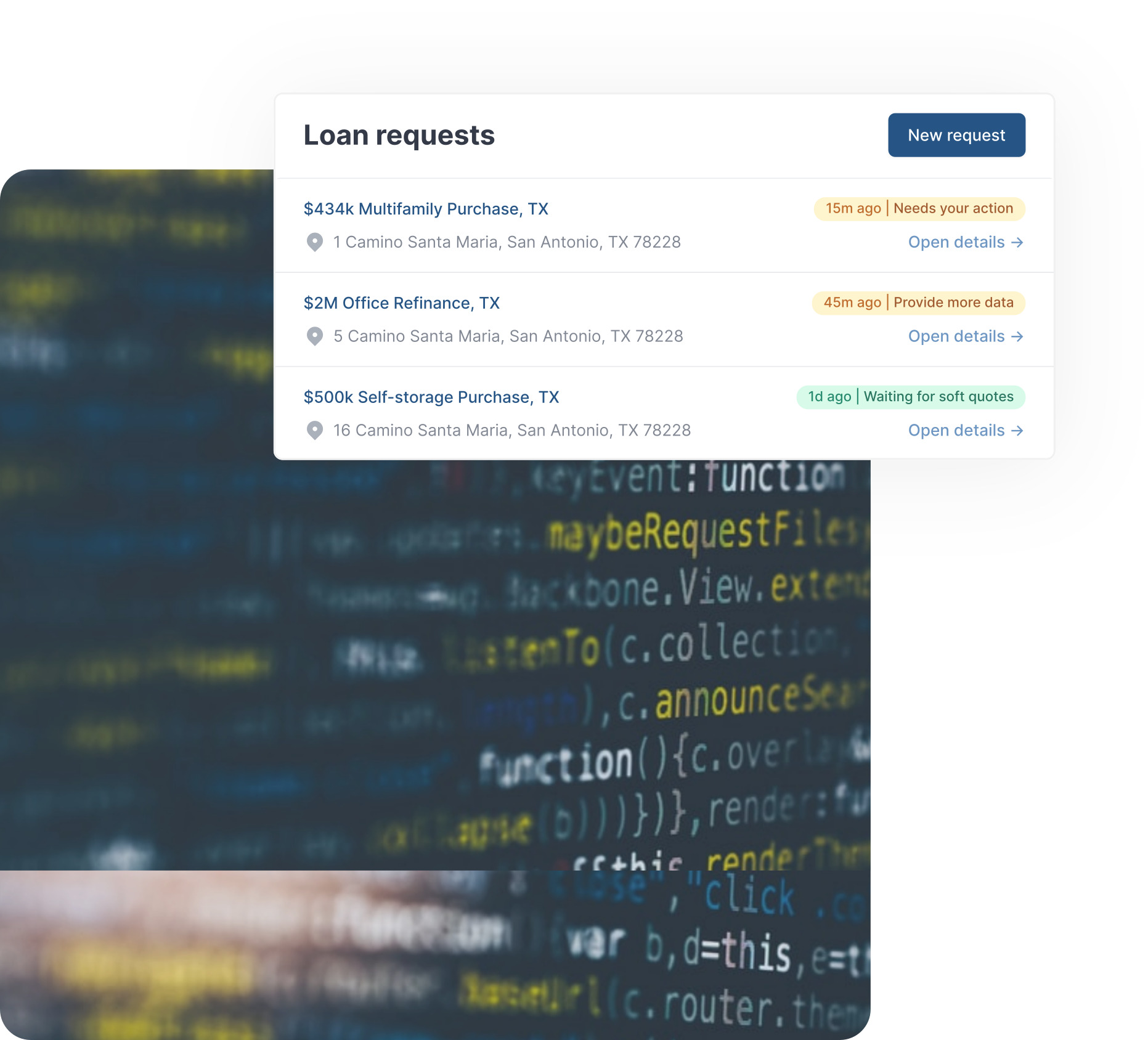

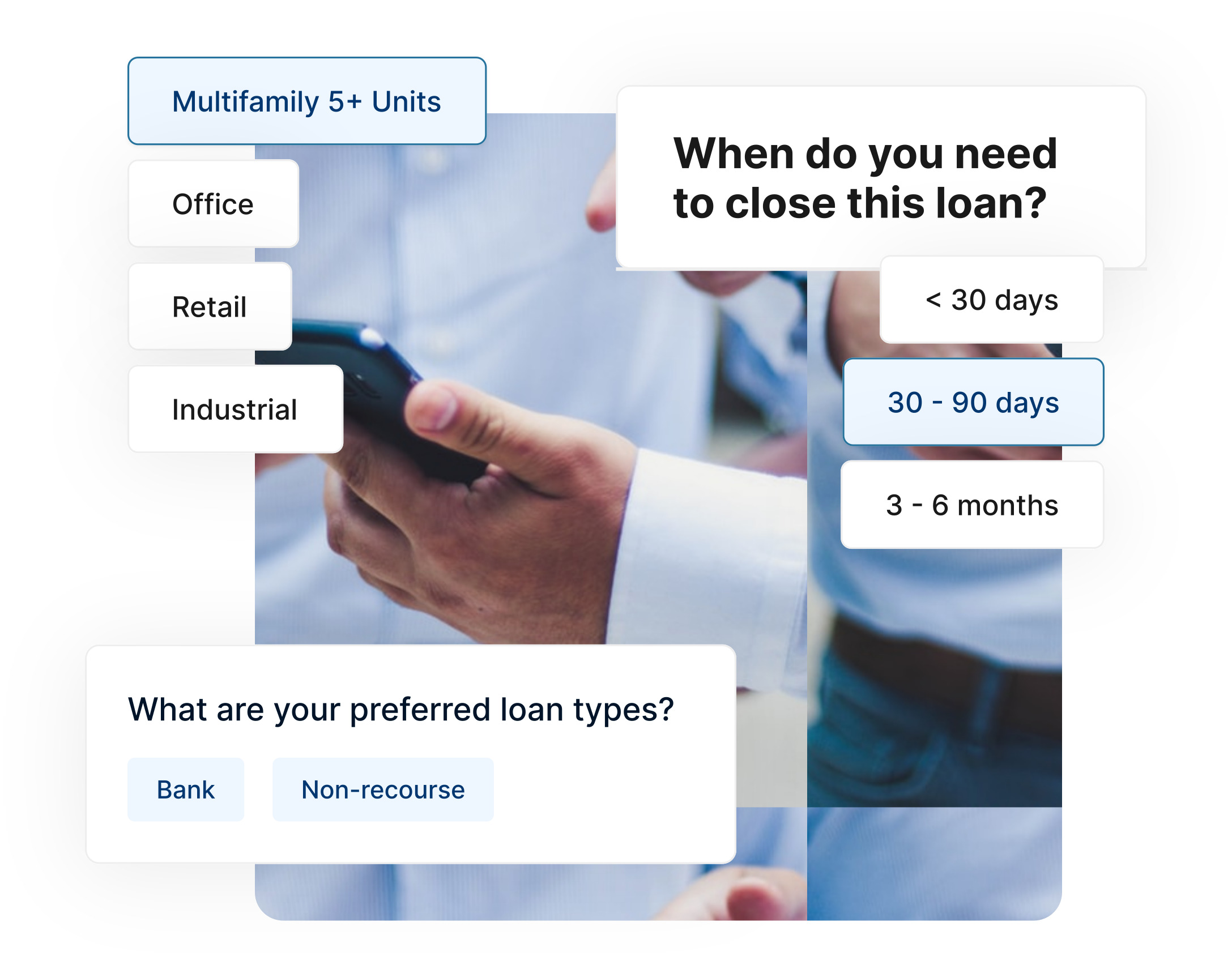

Let the industry’s best Commercial Real Estate property loan financing come to you. Fast loan application Breeze through easy-to-answer questions about your prospective loan then get funded.

Powerful matching

Let us find the needle in the haystack.

We match you with the best financing offers from lenders looking for deals like yours.

Smart document management

Streamline your workflow and upload documents seamlessly across all of your active deals.

Expert guidance

Get full transparency into every offer and compare options easily, with industry-leading tools and access to a team of experienced capital markets advisors.

One platform,

limitless potential

For borrowers of all sizes and every type of loan product — from a simple refinancing to a complex multi-tiered capital stack.

Agency Multifamily — Fannie Mae & Freddie Mac

Agency is a broad market for multifamily capital. It deserves a lot of attention and an incredibly deep understanding of the space in order to be navigated effectively. There are a multitude of products between Fannie Mae and Freddie Mac; from DUS, to conventional, to SBL and back. Each program has its own strengths and weaknesses and although many stabilized multifamily deals may fit in both buckets, sometimes one is far better than the other for pricing, execution, leverage, a little i/o, or all of the above. It is important to work with a shop that understands the nuances of agency debt to help borrowers achieve tighter margins and improved execution.

Our focus is bringing institutional leverage, pricing, and execution to small and middle market multifamily investors with a hyper focus on loans between $750k and $7MM. Our capabilities allow for loans up to $100MM or more, but we believe we add the deepest value to the small balance industry by educating and executing. Although we pride ourselves on our ability to close large and complex capital markets transactions, the core of our business is empowering the risk-managed growth of our first time agency borrowers.

FHA Multifamily

Some of the most competitively priced financial instruments with the most aggressive terms in the industry are FHA-insured multifamily loans. With leverage on both permanent and construction debt up to 85% LTC for market-rate products (and higher for affordable, LIHTC, RAD, etc.), non-recourse terms for up to 35 years for existing assets and 40+ years for permanent construction loans (not to be confused with construction-to-perm), terms and leverage are always superior to “market.”

Rates, including MIP (mortgage insurance premium), are generally lower than all other loan products, besides perhaps some life company debt, because of the government guaranteed default insurance on the loans. For inexperienced borrowers, lenders, and intermediaries, arranging FHA debt can be a daunting path to navigate due to its inherent complexities, but we pride ourselves on our FHA multifamily strength and as such, are a market leader. From $1MM to $100MM+ HUD®-insured multifamily loans lead the industry in terms but require the right team for execution quality to match product strengths.

CMBS

Not all CMBS loans are created equal, and neither are the lenders. We are highly focused on small CMBS debt between $2MM and $7MM where fees run high, and we have the ability to manage the costs and process more efficiently than the nation’s biggest banks and CMBS lenders. When it comes time to negotiate an assumption, to pick the right legal counsel or get the tightest spread, relationships and product-education matters deeply.

Some CMBS lenders favor one product one month and the next month are pricing that same asset-class wider than everyone else. A finger on the pulse of the market is required to know, for example, where you can capture the most i/o and lightest third-party costs while still achieving maximum execution. How many CMBS lenders does your broker work with?

Banks & Credit Unions

Although bank debt is often considered the debt of last-choice to some of the more institutionalized or experienced borrowers (because of shorter terms, amortizations and recourse provisions) they are still the go-to for other shops (both big and small alike) for lots of reasons. The reality is that they quite often offer the lowest cost-of-closing and (with some level of recourse for loans under $10-$20MM) sometimes the lowest rates (relative to leverage). They also have a very important feature that lenders who scrutinize their debt don’t have—the ability to reduce or even eliminate prepayment penalties.

Bank and Credit Union debt can be wonderful for transitional and bridge opportunities as well. The reality though is that there are thousands of banks and credit unions making commercial mortgages. How do you choose the right one? You have to have the right commercial mortgage brokerage with the right relationships.

Construction

Arranging construction debt becomes far more granular as submarkets have their own occupancy trends, cap rates, absorption rates, concessions, and much more. Financial modeling for construction loans becomes even more nuanced when calculating IRRs based on various exits, stress-testing permanent debt, and creating an efficient capital stack. Everyone from FHA to life companies to banks play in the construction space in one capacity or another and when it comes to arranging construction debt the diversity of relationships is as important as the depth of them and the experience of the advisor running lead on the transaction.

Construction financing is a field that requires an understanding of the entire geographical market as well as specialized know-how for construction of individual asset classes.

SBA

It is in the very mission statement of the Small Business Administration to help Americans start, build, and grow businesses. The Small Business Administration is tasked with aiding, counseling, assisting, and protecting the interests of small business concerns, preserving free competitive enterprise, and maintaining and strengthening the overall economy of our nation. To that end, when small business owners and entrepreneurs of all industries need to seek financial assistance or supplemental funding to help grow their business, one of the best ways to secure that funding is with an SBA loan.

The SBA sets guidelines and works closely with lenders in order to secure loans for small business owners. They do not originate or service these loans. Instead, they guarantee the funding amount in order to minimize the risk to the lender, which in turn makes obtaining flexible financing much easier for small business owners.